Obtain free International Economic system updates

We’ll ship you a myFT Each day Digest electronic mail rounding up the most recent International Economic system information each morning.

The marketplace for US Treasuries has gotten fairly ugly previously week, with the 10-year yield rising to its highest ranges since 2007.

Final week’s projections from the Federal Reserve satisfied buyers the US central financial institution actually gained’t be slicing charges or loosening coverage any time quickly. In the presser, Fed Chair Jay Powell mentioned he “wouldn’t” name a comfortable touchdown his “baseline expectation” (although it’s “believable”), and that progress “could also be determined by components which can be outdoors our management.”

Since then, 10-year Treasury yields have achieved this:

That’s a screengrab of twenty years of historic information from FactSet, as a result of some strategists have began to speak in troublingly historic phrases.

One of many louder warnings comes from JPMorgan strategist and vol whisperer Marko Kolanovic. This one carries the alarming subhed of “rates of interest — historical past doesn’t repeat, however it rhymes with 2008”.

He’s been fairly bearish this 12 months, and is remaining that manner (along with his emphasis):

With the current market decline, our 12 months finish value goal of 4200 set on the finish of final 12 months was reached (market is presently ~1% above our goal). Whereas the S&P 500 remains to be up for the 12 months, the positive factors are solely from a handful (7-8) of mega cap tech shares, impressed by the AI narrative, and defying the sharp rise in rates of interest. Maybe a greater gauge of macro-fundamentals is the S&P 500 equal weighted or small capitalization indices which can be flat for the 12 months and are underperforming money (Fed Funds). Why haven’t we modified our defensive stance, and what may come subsequent? Regardless of the sturdy early-summer rally, our framework continues to level to difficult macro fundamentals and headwinds for dangerous property. This reasoning relies on market valuations (fundamentals), investor positioning, and varied macro and geopolitical concerns.

Over the previous 6 months, the headwinds for dangers in our framework are stronger, and tailwinds weaker, in our view . . .

The core danger for markets and the economic system is tied to the rate of interest shock of the previous 18 months.

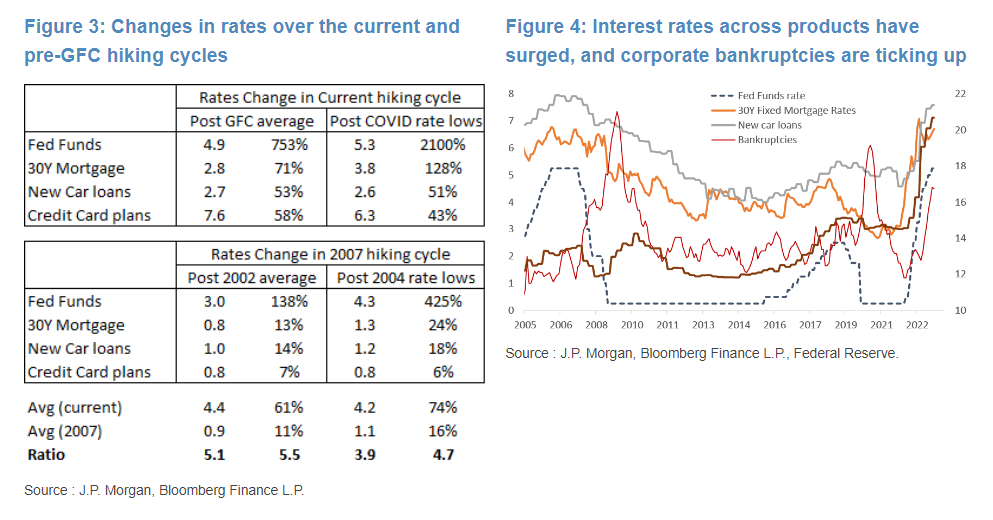

Determine 4 beneath reveals rate of interest change for Fed funds, mortgage charges (30y mounted), new automobile loans, and bank cards over the previous 20 years. Determine 3 reveals the present change relative to submit 2008 (GFC) averages, in addition to the ~2 12 months change from post-Covid lows. These shopper mortgage charges have elevated by ~4 proportion factors, which is roughly a 60-70% improve for these funds. Now we evaluate this improve to the rise that occurred in 2007 main into the GFC. In comparison with the pre-GFC common (since 2002), shopper charges elevated by about 1 proportion level, roughly a ~15% improve. So the present change in rates of interest is about 5 instances bigger than the 2002-2008 improve. After all, shopper stability sheets and leverage in actual property markets and the monetary trade have been larger going into 2008, however buyers ought to fastidiously monitor the propagation of the rates of interest shock throughout markets and completely different segments of the economic system.

Within the charts beneath, Kolanovic highlights the unusually speedy tempo of charge will increase, together with the rising price of debt throughout the broader US economic system:

Click here for a much bigger model. (Warning: he does commit the chart/desk crime of calculating the share change of an rate of interest, however he contains percentage-point change as nicely.)

{kind=link}

Strategists at Financial institution of America say that whereas long-dated Treasury yields may maintain rising, the :

Submit COVID = there isn’t any various (TINA). Immediately = there are various options (TAMA). USTs are an more and more compelling various to danger property, in our view.

We anticipate US charges to maintain rising till adverse suggestions from (1) actual financial slowdown (2) danger property, or (3) sufficient cuts are priced out — which might additionally comprise the sell-off. US charges have risen sharply on account of: (1) resilient US information (2) daunting provide / demand backdrop (3) stretched UST positioning. All of this has led to 75bp of 2024 cuts as an alternative of 150bp in July. The current sell-off was catalysed by the Sept FOMC. Powell probably just isn’t assured that charges are sufficiently restrictive; probably larger US charges until they chew. Our backside line: the trail of least resistance is larger charges and steeper curve.

And TS Lombard reminds us that every one of that is occurring as world central banks proceed to shrink the dimensions of their bond portfolios:

The affect of QT is hotly debated, however somebody wants to purchase that additional provide. The Fed board of governors has estimated that decreasing the stability sheet by round US$2.5trn over a number of years can be roughly equal to a 50bp hike (the discount to date is round US$1trn). Nevertheless, it additionally emphasised the “appreciable uncertainty” of the mechanical hyperlink of that estimate. One other viewpoint is that QE is basically a signalling software, ie, the ECB is utilizing it now to increase the cycle. That is an inside debate we now have had at TS Lombard. Regardless, the shift from QE to QT signifies a price-insensitive purchaser being faraway from the market and that debt must be purchased by somebody. So, who’s shopping for all of the debt? . . .

They discover that “actual cash” buyers, hedge funds and US households have stepped in, as seen within the chart beneath. That is in fact a bit tough to parse as a result of hedge funds and households are (comically) in the identical class:

TS Lombard strategists Skylar Montgomery Koning and Andrea Cicione proceed:

The provision/demand stability has put upward stress on yields. As we wrote throughout the summer season’s bearish FI storm, US issuance contributed to the surge in yields because it stunned the market in two methods: the sheer measurement of the deficit and the quantity of issuance that required; and the maturity profile of the debt being issued, with extra coupons than anticipated as T-bill issuance reached the share share of issuance that TBAC has set as a restrict. However that shock has been digested and yields are actually at enticing ranges. By the identical token, central banks’ stability sheets are nonetheless being drawn down, however the delta is not adverse (ie, the 12m stability sheet change is adverse however just isn’t getting any extra adverse). There was one thing of a relationship between Fed liquidity and yields YTD however pulling out the graph to an extended timeframe makes the case tougher to argue.

Oh and together with all of that issuance, there’s a US government shutdown looming. It isn’t clear precisely how that may have an effect on charges, although; previous authorities shutdowns haven’t moved the needle a lot, however they largely occurred within the ZIRP period, as strategists level out.

Earlier than wrapping up, we must also point out that Kolanovic pulled a 2007 technique notice out of JPMorgan’s archives, and located some similarities. We are going to admit to feeling burnt out on historic comparisons, after the recent resurgence of disco fever within the financial industry.

However he revealed the factor in full and added emphasis to the elements he finds related, so we are going to let readers decide for themselves:

“If financial efficiency in 2007 unfolds as our economists forecast, we expect the market is simply partway via what may show to be a difficult interval of transition. In our view, a change within the psychology surrounding the credit score markets began in mid-2006 and can carry over later in 2007:

Part 1: June-August 2006. The Fed institutes its final charge hike on June 30, 2006, lifting the fed funds charge to its present 5.25%, a transfer many thought was overkill. The Fed formally pauses on the August FOMC assembly and dangerous property embark on a robust rally that not solely lasts via year-end however carries over into early 2007. Nevertheless, the economic system is slowing perceptibly in response to a cumulative 425bp of mountain climbing over the previous two years, demonstrated by the decline in GDP from 5.6% in 1Q06 to 2% in 3Q06. A market consensus kinds across the view {that a} quickly slowing economic system and a pointy correction in residential housing valuations will pressure the Fed right into a sequence of charge easings. With the advantage of some hindsight, we’d additionally name this the “denial” part.

Part 2: December 2006-January 2007. The economic system offers compelling proof that it’s extra resilient than many had earlier believed. The sturdy December nonfarm payroll report opens sceptics’ eyes in regards to the underlying power of the economic system, and the renewed momentum is confirmed as financial information over the stability of December 2006 and January 2007 present an economic system shaking off the consequences of upper rates of interest and excessive commodity costs. Market contributors hand over the ghost on their hopes for easings, settle for that the Fed has engineered a comfortable touchdown, and purchase (actually) into the view {that a} Goldilocks economic system is within the making. Financial progress is stable at round 3% and led by a reinvigorated shopper; the residential housing sector slowly stabilises; company earnings progress moderates however doesn’t collapse; and inflationary pressures ease off however don’t dissipate. Dangerous property commerce at full valuations and stay in a slender, low vol vary. We’ll name this the “head pretend” part — all the things feels too good to be true as a result of it’s. In case you didn’t discover, that is the place we’re proper now.

Part 3: June-October 2007. Inflationary pressures ought to show persistent because the wholesome tempo of financial exercise places incremental stress on labour markets and utilisation charges. Market contributors now will start going through the painful realisation that the Fed will probably be compelled to lift rates of interest to comprise inflation. Nevertheless, earlier than any transfer to lift rates of interest, the Fed will intensify its hawkish rhetoric in an effort to arrange the market. Some buyers will take notice and scale back danger whereas others name the Fed’s bluff, stubbornly clinging to the view that housing, the buyer, and excessive leverage within the system can be authentic excuses for the Fed to carry off. Threat appetites subside, sentiment deteriorates, and valuations of dangerous property appropriate. The Fed goes forward and hikes anyway. On the danger of sounding smug, we are going to check with this because the “We instructed you so” part. If, as we challenge, progress fears proceed to recede and inflation considerations steadily improve, we expect it is just acceptable that danger takers ought to anticipate a part of valuations instability occasioned by a Fed that’s decided to maintain inflationary stress inside its nicely articulated targets. Our greatest guess is that such a part may emerge later this 12 months, presumably throughout the third quarter.”

Assist for and/or gripes about this 2007 comparability, as at all times, are welcome within the feedback.