Obtain free Demographics and inhabitants updates

We’ll ship you a myFT Each day Digest e mail rounding up the most recent Demographics and inhabitants information each morning.

“May you live in interesting times” is just not truly an outdated Chinese language curse. Nevertheless it’s awfully tempting to make use of it when writing about China’s financial system nowadays.

The phrase more and more used to explain its predicament is Japanification — a protracted painful stretch of actual property woes, deleveraging, financial stagnation and deflation. We wrote a chunky post about it here.

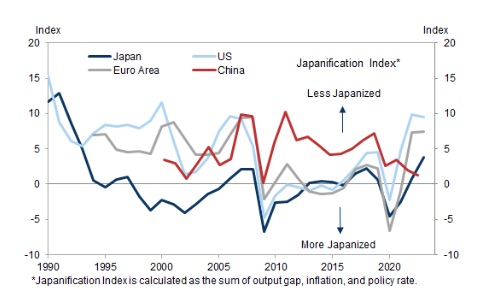

Again in 2016, professor Takatoshi Ito of Columbia College designed a easy “Japanification index” consisting of the sum of the output hole, the inflation price and short-term rates of interest In different phrases, the decrease the rating, the extra Japanese you have been.

Remarkably, by this measure China is now extra Japanese than Japan, as this chart from Goldman Sachs reveals (zoomable version):

{kind=link}

Goldman’s economists undergo most of the identical parallels and variations between Japan within the Nineties and China at present as JPMorgan did in report we wrote up final month.

However they depart in a single attention-grabbing space: demographics truly matter little to Japanification, whereas expectations issues rather a lot.

Japanification is often seen as an financial state of affairs the place deteriorating demographics trigger structurally low development, inflation, and rates of interest. Probably the most intuitive channel is through declines in labor enter. Nevertheless, regardless of going through this problem, Japan’s financial system nonetheless grew modestly over the last decade (apart from the pandemic interval), leading to a notable decoupling of financial exercise from the steadily declining working-age inhabitants . . .

. . . Japan’s expertise means that demographics will not be as necessary as many suppose relating to Japanification. In China, the retirement age is 60 for male staff and 50 or 55 for feminine staff. Even after contemplating casual employment past official retirement age uncaptured by the official statistics, there ought to nonetheless be room for labor provide to broaden, if wanted, by rising the retirement age. As well as, the rise of AI and its potential to switch staff could additional cut back the significance of labor in driving financial development sooner or later.

In contrast, the expectations channel — specifically, the downward stress of demographics on long-term development expectations amongst companies and households — was probably extra necessary than simply bodily shortages of labor enter in driving “Japanification” . . . When deterioration in demographics appeared more likely to proceed, it lowered expectations of future development potential for the Japanese financial system as a complete and thus anticipated lifetime earnings. The necessity to deal with debt overhang amongst firms, as an aftermath of the bursting of asset bubble, along with the preliminary sturdy forbearance stance from each banks and the federal government (mentioned additional under), amplified this from a monetary perspective. Such lowered earnings expectations depressed spending on consumption and funding, which in flip ushered in a unfavourable suggestions loop.

After all, this isn’t essentially excellent news for China!

It’s fairly clear that individuals have turn into a LOT extra pessimistic over the previous 12 months, with slumping enterprise investments, grim shopper confidence readings and falling financial development forecasts.

Beijing appears decided to handle this disaster of confidence by what could be termed the ostrich approach, ordering local economists to be more positive and discontinuing awkward data sets and so on.

{kind=link}

Goldman argues that there may be a greater strategy to stop the present downturn from morphing into one thing nastier.

In our view, extended pessimism and continued downward shift in longer-term development outlook, particularly with worsening demographics and debt overhang within the background, are extra threatening to China’s financial prospects than working-age inhabitants development per se, as demonstrated by Japan’s expertise. To circuit-break additional deterioration in development expectations, the federal government could think about emphasizing the significance of financial growth, accelerating the restructuring of troubled property builders and native authorities financing autos to chop off left-tail dangers, and strengthening social security nets to encourage family consumption over the long-run.

. . . Along with managing longer-term development expectations, there are three different cautionary tales for Chinese language policymakers. First, coverage predictability and coordination are necessary for funding demand from the non-public sector, the dearth of which may push the Chinese language financial system additional alongside the Japanification path even within the absence of asset bubble burst. Second, monetary establishments’ skill to lend must be protected and Japan’s expertise suggests industrial banks shouldn’t be made the only absorber of NPLs within the means of property deleveraging and native authorities implicit debt cleanup. Third, deflationary insurance policies similar to wage-cutting needs to be used with nice warning as they might danger making a wage-price downward spiral that resets inflation expectations decrease and makes debt deleveraging excessively painful.

Additional studying

— The great Chinese flow reversal

— China’s housing market is . . . not good

— China’s Japanification

— The implications of China’s mid-income trap