Obtain free Free Lunch updates

We’ll ship you a myFT Day by day Digest e-mail rounding up the newest Free Lunch information each morning.

This text is an on-site model of Martin Sandbu’s Free Lunch publication. Join here to get the publication despatched straight to your inbox each Thursday

Greetings. Thrilling information from the FT’s steady of newsletters: our long-serving economics editor Chris Giles is transferring to a brand new position protecting central banks. His publication, which can exit each Tuesday, will deliver the kind of intelligence you anticipate from the FT, which is essential when massive questions confront financial policymakers and those that rely upon their selections — which, let’s be sincere, is all of us. So please sign up to present Chris Giles on Central Banks a strive.

The shift in EU fascinated by commerce coverage has been positively whiplash-inducing. Brussels has gone from being an (nearly) dedicated free dealer — which was itself a welcome change from a dominance of corporatism and agricultural protectionism within the EU’s early many years — to being dominated by a geostrategic view of worldwide commerce. The approval in member state capitals has ranged from grudging to enthusiastic.

That’s not a foul factor — it’s clear that some commerce hyperlinks had been weaponised by geopolitical adversaries to make the EU and its member states depending on them. That was true for fuel pipelines with Russia, and it may grow to be true wherever China is a monopoly provider of vital items. However it’s one factor to understand the risks one faces and take the very best steps to get rid of them. It’s fairly one other to overreact and rush for a response that finally ends up being each costlier and fewer environment friendly than it must be. The EU and its member states may do properly with a bit extra of the previous and a bit much less of the latter.

A working example is the present concern concerning the bilateral commerce stability. The EU’s trade deficit with China has roughly tripled in 5 years, inflicting a lot harrumphing among EU trade officials and little question strengthening protectionist emotions.

It’s a primary lesson of worldwide economics that bilateral balances vis-à-vis explicit international locations matter much less (if in any respect) than an financial system’s total exterior stability. However financial irrelevance has by no means been a hindrance to political salience. In any case, such an enormous change in so little time is kind of breathtaking, so it’s price checking what’s behind it. Listed below are the important thing information.

First, the ballooning bilateral deficit is solely pushed by an increase in imports relatively than a fall in exports. Because the chart under reveals, the 2 grew kind of in parallel on the finish of the final decade. Then, after the primary lockdown-related swings, EU exports to China remained kind of steady, whereas imports soared.

Second, the change in imports is seen throughout broad classes of producing, though equipment and transport gear (consider China’s electrical automotive growth) could also be contributing greater than its proportionate share.

Third, the EU’s bulging Chinese language imports invoice has as a lot to do with the imports’ value than their quantity. From June 2021 to September 2022, the unit worth of the stuff the EU purchased from China rose 30 per cent, whereas that of the products despatched the opposite approach solely rose 18 per cent. Even when commerce volumes had stayed fixed, this terms-of-trade shock would have made the deficit deteriorate considerably. Not that that is nothing to fret about; it clearly made the EU poorer. However it’s growing volumes of products purchased that may point out a deepening dependence.

Import volumes grew too, after all, if not as a lot as costs. However fourth, and most significantly, all these modifications have lately been going into reverse. Import volumes have fallen by about 10 per cent because the peak in August final 12 months; import costs by about 15 per cent. The whole import invoice, consequently, is down by a about quarter since a 12 months in the past. Exports, in the meantime, have been steady in each nominal and actual phrases over the identical interval. That also leaves the deficit so much increased than earlier than the pandemic. But it surely doesn’t do to make use of 2022 numbers as justification for coverage.

This is only one instance of the place nuance is essential in order to keep away from knee-jerk coverage responses to momentary or oversimplified challenges. And fortuitously, such nuance is forthcoming within the debate. Listed below are two examples which have come throughout my desk previously week.

One of many fears in Europe is that China may use its dominance within the vital uncooked supplies that inexperienced tech manufacturing is dependent upon, for geopolitical functions — and that concern is justified, as an interactive visual report from my colleagues brings dwelling. And but: in a letter to the FT, the economist Daniel Gros has identified the curious indisputable fact that the worth of EU imports of uncommon earths just isn’t that prime ($121mn in 2021, he says). He argues that this implies it’s extra inexpensive to stockpile vital uncooked supplies than to plough billions into subsidies for his or her home extraction. After all, China might restrict gross sales to forestall exactly that, or the demand would possibly rocket so excessive that there’s nothing left to stockpile. But it surely nonetheless places the geopolitical dependence into a distinct perspective and encourages us to consider extra coverage options.

One other instance is the European concern that the US will steal its inexperienced transition bacon. So I welcome a brand new notice from the Franco-German Council of Financial Specialists — which is made up of the 2 international locations’ government-appointed however impartial financial advisory councils — on how the EU ought to react to Washington’s Inflation Discount Act. That piece of laws, you’ll recall, has helped gas a growth in manufacturing facility development within the US, and was acquired with horror by European politicians who had been advised by their industrialists that with the brand new American subsidies they’d up sticks and shift their investments throughout the Atlantic.

The joint crew of financial sages are telling their governments to relax: the IRA won’t have a big impact on the EU financial system. Even within the particular sectors the place new US subsidies are making companies ponder if the grass is greener on the opposite facet of the Atlantic, there isn’t any proof of “vital dangers for the EU”. The explanations embrace that the IRA largely simply makes the US meet up with the subsidies the EU already provides, which the report paperwork, and that the EU’s reliance on carbon pricing makes any given quantity of subsidy far more efficient. General, the conclusion is that the majority of inexperienced tech might be consumed inside the identical financial bloc the place it’s produced, so there may be not that a lot scope for subsidies in a single bloc to upset exercise within the different.

None of this implies Europe shouldn’t fear about its dependence on different economies. However its leaders ought to suppose extra broadly about coverage options, making an effort to study when the scenario just isn’t fairly as dire — or easy — as it could have served their curiosity to inform voters. Above all, don’t panic. It doesn’t make for good coverage.

Different readables

Numbers information

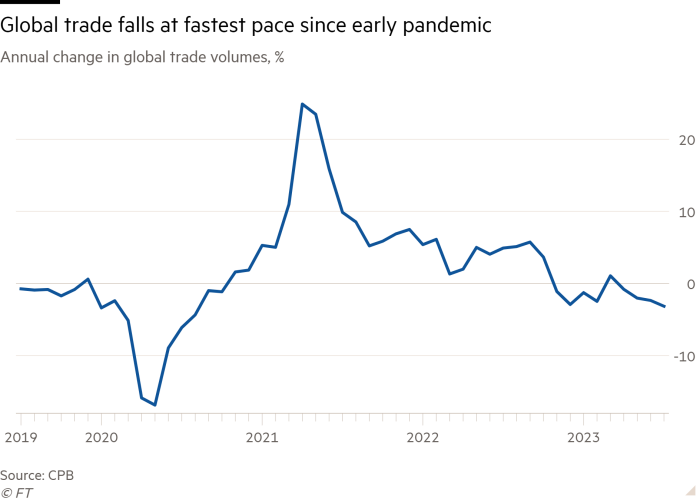

-

Global trade is shrinking on the quickest tempo because the early pandemic on a year-on-year foundation.

-

The Kyiv Faculty of Economics has printed its newest chartbook on the impact of sanctions on the Russian financial system.